The CX dividend: A missed revenue opportunity for insurers

As acquisition costs rise, insurers are focusing on pricing while neglecting CX that determines long-term value

The CX dividend: A missed revenue opportunity for insurers

As acquisition costs rise, insurers are focusing on pricing while neglecting CX that determines long-term value

- UNRVLD works with insurers to accelerate their digital effectiveness to match the sophistication of their pricing operations: as both can quickly impact profit margins

- Experience, particularly digital CX, is an insurer’s unseen profit engine if they take the same approach to it as other digitally mature sectors such as retail, banking and travel

- Investment in the experience layer reduces acquisition costs, improves lifetime customer value and can also positively impact cost to serve

Every interaction a customer has with an insurer, from obtaining a quote to adjusting or renewing a policy or making a claim, now takes place through a digital experience designed, built, and deployed by someone. The quality of that experience determines whether a customer converts or abandons, stays or shops around, expands their relationship with additional products or drifts away entirely.

In sectors where the value of digital experience has long been understood - notably retail, banking and travel as three sectors where UNRVLD has digitally mature clients - the systematic optimisation of those journeys is a core commercial discipline. Brands continuously test, measure, and improve these experiences to establish an optimal outcome.

In UK insurance, however, this discipline largely remains underdeveloped. While pricing engines are treated as precision instruments under constant scrutiny, Customer Experience (CX), in contrast, is still treated as an operational afterthought, rather than a growth lever, and its commercial potential remains largely untapped. This gap is becoming increasingly costly, driving significant missed opportunities.

Pricing excellence, experience neglect

UK personal lines insurers have spent a decade building some of the most sophisticated pricing engines in financial services: boasting continuous model deployment, near real-time competitive monitoring, and pricing teams that have scaled faster than almost any other function in the business.

The investment has been significant and effective. Policy volumes are rising, and market share is increasingly concentrated among those who price most aggressively and precisely.

And yet, operating ratios are deteriorating.

The reason is not difficult to diagnose. Acquisition costs, largely price comparison commissions, increase with every new policy. Meanwhile, premiums are softening as competition intensifies. These two forces compress margins from both sides, and pricing sophistication alone cannot resolve this structural squeeze. It can only optimise within it - continuing to deliver customers, but at an incrementally higher cost per policy acquisition, resulting in a gradual erosion of underwriting profit.

The result is a business model that is increasingly efficient at acquiring customers, and increasingly expensive to do so. The value of each customer post-acquisition has therefore never been more important. That value is largely determined by the quality of the customer experience layer. Yet in most UK insurers, the experience layer is not managed with anything close to the same discipline applied to pricing.

The CX dividend is already embedded in operating ratios. The question is whether insurers are positioned to realise it... or even aware it exists.

Operational asymmetry

Consider how UK personal lines insurers approach pricing.

Behaviour is more akin to modern technology companies. Every competitive position is modelled, tested, and iterated. Changes deploy in hours. Feedback loops between data and decision are continuous, and measurable. Entire teams exist to ensure that the price a customer sees reflects the latest view of risk, competition, and margin.

Now consider the customer experience layer.

Quote journeys are typically designed once and then infrequently iterated, if at all. The renewal experience is largely identical regardless of customer value or product breadth. Cross-sell prompts: motor to home, single to multi-car, are generally static rather than driven by behavioural signals.

Self-service journeys were introduced to reduce call volumes, but in many organisations, it is not rigorously measured for whether they do, by how much, or what cost they remove from the operating model. Meanwhile, content across product lines and sub-brands is often managed manually, inconsistently, and without clear governance despite operating in a highly regulated industry.

This gap between pricing discipline and experience discipline matters.

This is not a maturity gap, but a misallocation of attention and investment. Pricing has been industrialised, while experience remains under-optimised despite carrying comparable economic weight.

The distinction matters commercially, because the marginal gains from further optimisation of the acquisition funnel alone are limited.

An insurer acquiring four million customers via price comparison pays commission on each one. Improving quote-to-bind conversion by half a percentage point reduces acquisition cost at the margin. It is worth doing, but it does not change the underlying economics.

The real leverage sits elsewhere.

An insurer whose existing motor customers add home insurance at twice the current rate is growing a product line at almost no additional acquisition cost. A one percentage point improvement in renewal rates retains tens of thousands of customers without re-acquisition spend. Self-service journeys that genuinely reduce call volumes and appropriately manage customer needs, take cost directly out of the operating ratio, rather than merely improving conversion.

The experience layer does not merely support the acquisition engine. At current UK personal lines scale, it is the more powerful lever. Improvements in cross-sell, retention, and service efficiency compound without incurring the same acquisition costs that are driving operating ratios upward.

These are significant structural gains.

The acquisition funnel brings customers in and the experience layer determines whether the economics of keeping and growing them actually works.

The hidden divergence

We see a consistent pattern emerging across large, multi-brand insurers: optimisation effort gravitates towards the flagship journey. It has the dedicated teams, the scrutiny, the tooling, and the commercial pressure to justify constant refinement and iteration. Everything else - secondary brands, newer product lines, renewal flows, and self-service journeys - typically operates on inherited assumptions, established at launch and refined only intermittently.

The result is a divergence in performance that is almost entirely invisible at group level.

The group operating ratio is a blended metric that masks this variation, as it aggregates highly optimised journeys that suppress cost and improve conversion with under-optimised journeys that do the opposite.

The optimised core pulls it down. The un-optimised journeys - renewals that haven't been tested across brands, cross-sell paths that exist in theory but aren't measured, self-service flows that were launched functional but never improved - pull it up. And because reporting sits at group rather than journey level, this spread and the extremes are largely obscured..

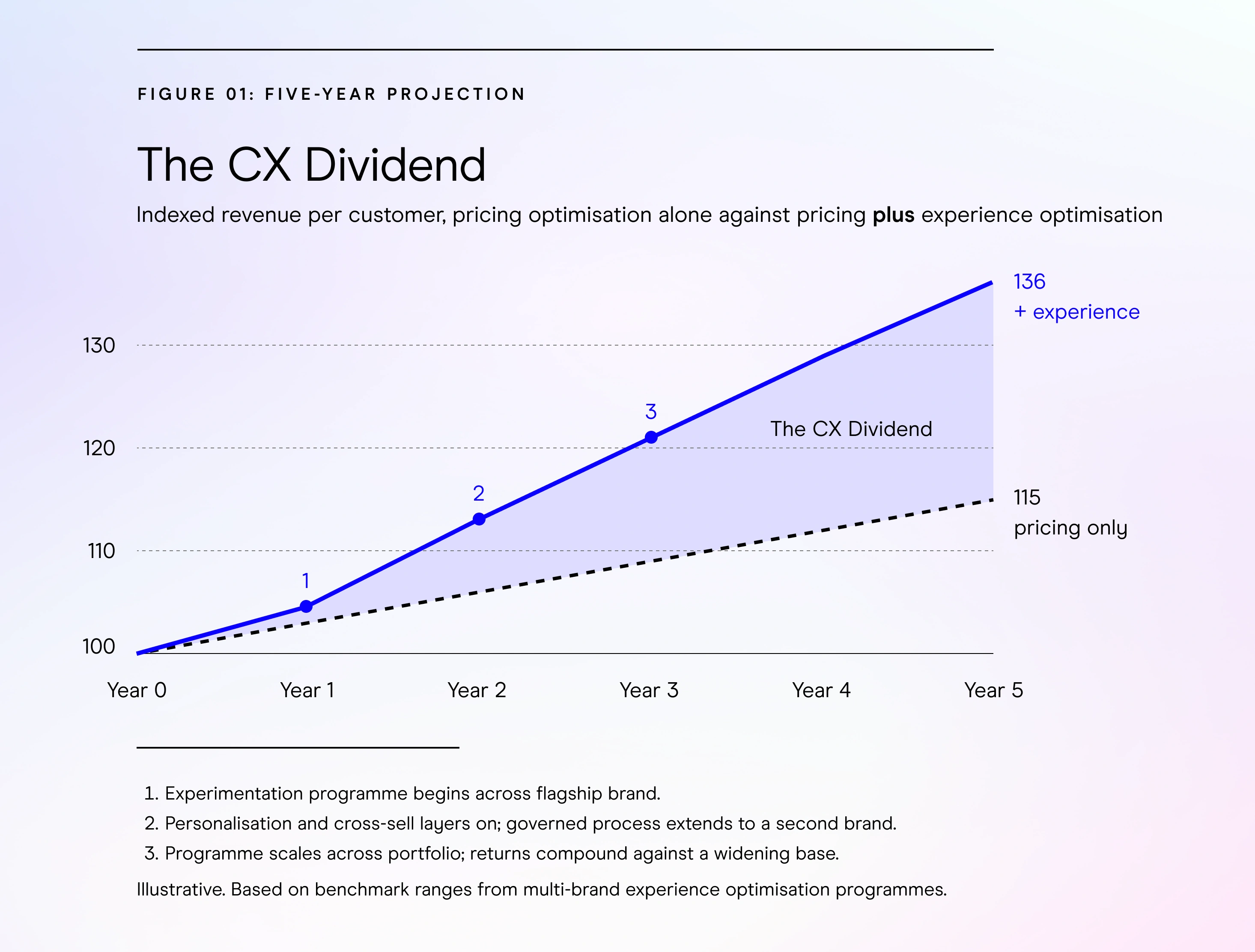

What happens when digital experience is treated as a system?

Quite simply, where organisations extend disciplined optimisation beyond a single journey, the returns are rarely marginal, as the above graph demonstrates.

Our work with multi-brand organisations that have extended a governed optimisation capability from the primary brand to the wider portfolio has boasted returns that dwarfed the original programmes.

In one multi-brand enterprise, scaling experimentation and personalisation across the full portfolio delivered a 15:1 return on investment and generated tens of thousands of additional qualified leads in just eight months, by extending the programme beyond the flagship and across the wider brand portfolio.

In a regulated financial services organisation, re-imagining and digitising complex onboarding and self-service workflows materially reduced manual processing and improved cost to serve. And in a high-volume service business, end-to-end automation of a complex journey eliminated manual intervention entirely and lifted conversion volumes by more than 400% - far exceeding sales forecasts.

The mechanism is consistent. Returns compound when governance and optimisation is applied at portfolio level. Learning propagates as data flows and intelligence from one brand or journey informs the next. The programme gets smarter as it scales because the data, the methodology, and the learning are connected rather than siloed.

The insurer CX dividend in plain sight

One can only imagine the velocity and scale of optimisation if applied at the volume UK personal lines insurers experience.

The industry operates at enormous scale - larger than almost any other digital consumer category in the UK market. Tens of millions of quotes, renewals and service interactions processed annually. At that volume the opportunity is vast - small improvements in cross-sell, retention and service efficiency translate into material shifts in profitability.

And yet optimisation effort remains unevenly distributed. The industry has become highly sophisticated at acquiring customers but it is far less sophisticated at making them valuable once acquired.

At current scale, that imbalance is a huge constraint.

Compounding complexity: why the gap widens over time

What makes this a problem is this is not a static inefficiency. It worsens with growth.

Every new product added to the portfolio (home, van, bike, personal loans, telematics) creates new journeys that that need to be designed, tested and governed.

Every sub-brand that serves a distinct customer segment (essential, premium, young driver) introduces another surface that should be optimised but often isn't. Each year of content produced without a governance model accumulates atop a growing stock that is neither measured, tested, nor retired.

Growth, in other words, expands the surface area of under-optimisation.

An insurer growing at 15% a year is not simply getting larger. It is becoming more complex: more journeys, more brands, more content, more interactions running on launch-day assumptions. The flagship journey continues to improve. The rest does not. The gap between the two widens with every quarter.

The operating ratio therefore reflects more than today's cost structure and current performance. It reflects the accumulated consequences of where optimisation effort has, and has not, been applied. Every quarter of deferred optimisation across the portfolio is a quarter in which the gap compounds against a growing base.

The missed discipline

The question for any insurer examining its operating ratio is not whether the experience layer matters, but why it continues to be overlooked.

The pricing function already demonstrates what disciplined optimisation looks like: continuous testing, tight feedback loops, and decisions grounded in evidence rather than assumption. It delivers commercial impact every day.

So, one must question why that same discipline, the same rigour, the same feedback loops, the same insistence on evidence over assumption, has not been extended to the journeys that determine what each acquired customer is really worth.

The insurer who recognises this first can compound the dividend with every policy on the book.

Natalie Waite is Head of Experience Optimisation at UNRVLD, a digital experience agency that works with large organisations to build experience optimisation programmes across their multi-brand portfolios.

To understand what the experience layer could be worth to your business, complete the form below and we’ll arrange for an introductory call with Natalie and our other relevant digital subject matter experts.